Minister of Finance Enoch Godongwana opened the 2026 Budget Speech by noting a long list of challenges over recent years, including state capture, the pandemic, rating downgrades, grey listing, rising government debt and more.

As he noted, “warning lights were flashing” – but these multiple crises were turned into a catalyst for change.

Read: Best budget in years – but from a very low base

As a result of much-needed reforms, the picture is a lot better today, which makes the budget less of the “make-or-break” event it was in past years.

The country might be re-entering a period of boring budgets – which would be fantastic – though of course we are also now in the age of coalition governments, introducing a new dimension of uncertainty.

Partly for this reason, Treasury is finalising legislation that will bind future governments to long-term fiscal sustainability.

Read: Government wants a ‘credible and principle-led’ fiscal anchor

This so-called fiscal anchor will enhance policymaking credibility, much like inflation targeting gives clarity to monetary policy.

Global backdrop

It is easy to get lost in the myriad tables and charts of the budget and miss the broader context. There are at least four global elements to consider.

The first is the resilience in the global economic outlook, despite immense policy uncertainty coming from the US. Supply chain managers are again grappling with the implications of the recent Supreme Court ruling.

Read:

More tariff turmoil on the cards after US Supreme Court decision

Trump faces tough legal landscape to oppose tariff refunds

Trump’s 10% levy takes effect as US rebuilds tariff wall

US tariff turmoil creates strategic opening for SA

The International Monetary Fund projects growth of 3.3% this year, roughly the same as last year and in line with the long-term average. The war in Iran could derail this outlook, but it is really too soon to tell. A short-term spike in oil prices will cause little lasting damage, but a prolonged increase will put downward pressure on global growth and some upward pressure on inflation.

Secondly, and somewhat surprisingly, capital flows to emerging markets have increased, driven in part by a weaker dollar and a search for diversification on the part of international investors.

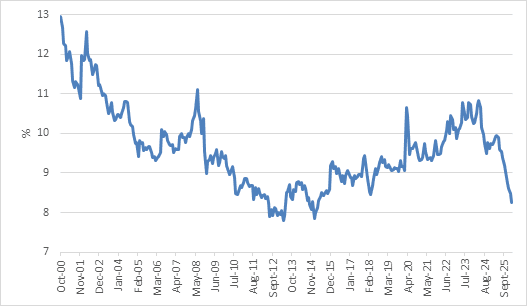

This has resulted in a compression of ‘spreads’, or the higher borrowing costs these countries must pay relative to the US and other developed countries. South Africa has been a major beneficiary of this, with the rally in local bonds further supported by last year’s formal shift to a lower inflation target, and with it, an outlook for structurally lower interest rates.

This delivered unprecedented returns from bonds for investors last year, but from the finance minister’s point of view, it results in significant long-term relief.

It can now borrow at around 2.5 percentage points less across the yield curve than at the time of the 2024 Budget and will also be able to roll over maturing debt at these lower costs. This is important specifically because there are significant maturities in the next three years.

National Treasury Director-General Duncan Pieterse noted that debt stock would be R277 billion lower by the 2029 fiscal year, compared with what was projected in the November Medium-Term Budget. This means that there will be less bond issuance, which should support bond prices all else being equal, and also significant savings on interest payments.

FTSE/JSE All Bond Index Yield, %

ADVERTISEMENT

CONTINUE READING BELOW

Source: LSEG Datastream

Thirdly, the surge in international precious metals prices, in part due to the global policy uncertainty, is a windfall for South Africa. The impact will not come through immediately, and corporate tax in the current fiscal year is only R7 billion more compared with earlier estimates.

Read: JSE breaks new record in budget week

But if gold and platinum prices remain close to where they are now, taxes from mining houses will rise considerably over the medium term. As expected, Treasury has been conservative in provisioning for this, leaving room for a positive surprise.

Fourthly, it is important to note that global public debt levels are rising relentlessly.

There are very few countries that are deliberately pursuing debt stabilisation strategies.

Consider the four biggest economies:

- The US debt outlook was worrying even before President Donald Trump took office. As a result of last year’s tax cuts and the possible reduction in tariff revenues, the picture is even worse.

- Germany was a poster child for fiscal discipline. In fact it took it too far, but is now massively increasing borrowing to upgrade its military and infrastructure.

- Japan’s new prime minister plans to do away with “mindless austerity”.

- China’s public debt levels are also very likely to keep rising as the national government extends support to boost the flagging economy.

Longer-term, each of these countries faces further debt implications from ageing populations.

In contrast, the South African government is on a debt-stabilisation journey after allowing debt levels to rise far too much between 2010 and 2020 (Covid caused another unavoidable jump in debt levels).

Unlike the four majors listed above, South Africa’s rapidly rising debt ratio since 2009 put significant pressure on its day-to-day finances, with an ever-larger portion of tax revenues devoted to interest payments because it borrows at much higher interest rates than the big four.

Even after the rally in SA bonds, the 10-year yield on SA government bonds is around 8% (compared with 4% in the US, 3% in Germany and 2% in Japan and China).

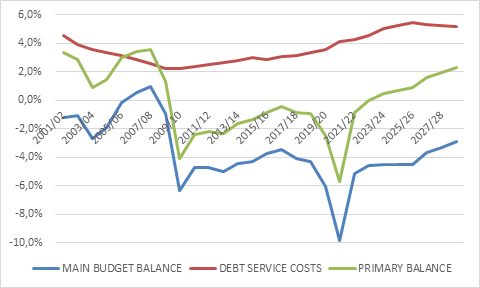

As the chart below shows, the debt service cost increased rapidly from 2% of GDP in 2010 to around 5% of GDP (fiscal numbers are usually expressed as a ratio of national income or GDP to allow for comparison across time and countries).

SA’s main budget metrics, share of GDP

Source: National Treasury, forecast after 2024/5

Stabilising debt levels and the associated debt service costs has required a politically difficult programme of constraining government spending while trying to raise tax revenues.

Since the 2024 fiscal year (ending in March 2024), non-interest spending has been held below revenues. The technical term for this is a surplus on the primary budget balance.

This primary surplus is projected to rise from 0.9% of GDP in the current fiscal year to 2.3% by the 2028 fiscal year.

As this happens, the deficit on the main budget balance should decline from 4.5% in the current fiscal year (ending March 2026) to 2.9% by the 2028 fiscal year. Yes, it would be much simpler if fiscal years aligned with calendar years.

ADVERTISEMENT:

CONTINUE READING BELOW

Peaking

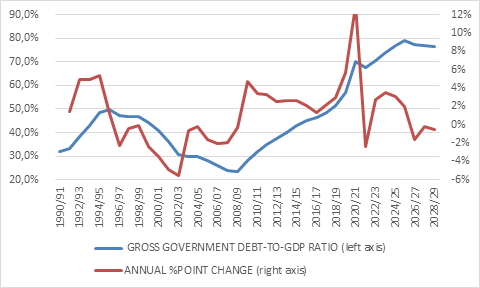

Meanwhile, the gross debt-to-GDP ratio is expected to have peaked in the current fiscal year at 79.8% of GDP.

For the first time in 17 years, the debt ratio will not increase, and is projected to gradually drift lower in the years ahead as the chart below shows.

If this happens, South Africa will increasingly stand out internationally, and in a world of rising debt levels, could see a further rerating of its markets and credit rating upgrades.

The chart also shows that South Africa has precedent for lowering its debt ratio. Between 1996 and 2008, under then finance minister Trevor Manuel (currently chair of Old Mutual), the debt-to-GDP ratio was halved, through a combination of fiscal discipline and the pre-2008 commodity boom.

South African government debt

Source: National Treasury, forecast after 2024/25

This can be repeated but will again require ongoing discipline and faster economic growth.

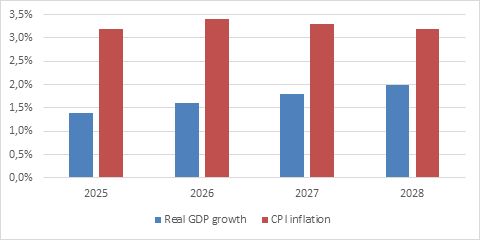

Treasury’s projections for growth and inflation are broadly line with most private sector forecasts and are therefore credible.

It expects real GDP growth to rise towards 2% over the medium term, not exciting by international standards, but notable by South Africa’s.

Household consumption spending is set to moderate from strong growth of 3.2% in 2025 to around 2% over the medium term.

Therefore, the growth uplift will come from fixed investment spending growth swinging from -2% in 2025 to 2.4% in 2026, rising to 3.9% by 2028. The increase in fixed investment spending by both public and private sectors is critical for the overall growth outlook and for fiscal sustainability.

Budget 2026 macroeconomic forecasts

Source: National Treasury

There was little new on this front in the budget, aside from reiterating the current programmes under way, particularly Operation Vulindlela, which has already delivered some key wins in crowding in private sector investments into areas previously monopolised by the state, notably electricity and logistics.

Treasury is also reforming the regulatory and institutional landscape to encourage public-private partnerships across different spheres of government to support infrastructure delivery.

The government’s own capex budget rises to R1.07 trillion over the medium term. This is part of an ongoing effort to shift from current spending (mostly salaries) to capital spending.

Read: Taxpayers’ wallets not enough to cover public servants’ paycheques

There is also an increased focus on improving the quality of overall spending, though this is an uphill battle. The Targeted and Responsible Savings (TARS) initiative has found R12 billion in savings over three years from programmes that deliver little value. This money will be reallocated, with further efforts underway to identify more savings.

ADVERTISEMENT:

CONTINUE READING BELOW

Some relief

There is little room to advance fiscal consolidation through further tax rate increases. We are surely close to the limit of how far the tax-to-GDP ratio, currently at 25.2%, can rise without being counterproductive and disincentivising economic activity.

A future value-added tax (Vat) increase remains a possibility – though it is not included in the 2026 Budget – but beyond that, higher tax revenues must come from faster GDP growth, not increasing the tax burden on individuals and companies.

Taxpayers received some relief in the budget.

There is compensation for bracket creep (the tendency for inflation to push people into higher tax brackets) for the first time in two years.

Meanwhile, small business owners benefit from the lifting of the Vat registration threshold to R2.3 million.

Read: Vat registration threshold updated for the first time since 2009

Notably, the R20 billion in tax increases proposed in the Medium-Term Budget Policy Statement (MTBPS) have been withdrawn thanks to the fact that tax revenues surprised on the upside.

Good better Budget

In summary, the 2026 Budget managed to be simultaneously dramatically different while maintaining continuity. What remains the same is macroeconomic and fiscal policy. The focus remains on debt stabilisation and boosting economic growth, with a strong emphasis on infrastructure.

What is very different is the market backdrop and renewed sense of confidence: bond yields have declined sharply since the previous budget, South Africa received a credit rating upgrade last year, and the rand has strengthened.

There is a bit of luck in this, notably the elevated precious metals prices.

But it ultimately reflects the fact that three reforms fell into place over the past few months, namely:

- The efforts of Operation Vulindlela, with strong steer from The Presidency;

- The lower inflation target; and

- The South African Reserve Bank’s steadfast policy credibility, as well as the culmination of years of hard work and tough trade-offs at National Treasury.

There are still many challenges and risks of course, but this can become a positive feedback loop, where improved sentiment supports rising investment, boosts economic growth and further reduces borrowing costs.

For South African investors, it means increased contribution limits to retirement annuities and tax-free savings accounts can be used with greater confidence, and that the policy landscape is providing much better support for future investment returns.

Read: Godongwana lifts annual TFSA limit

Izak Odendaal is an investment strategist at Old Mutual Wealth.

Follow Moneyweb’s in-depth finance and business news on WhatsApp here.

#Budget #pieces #falling #place