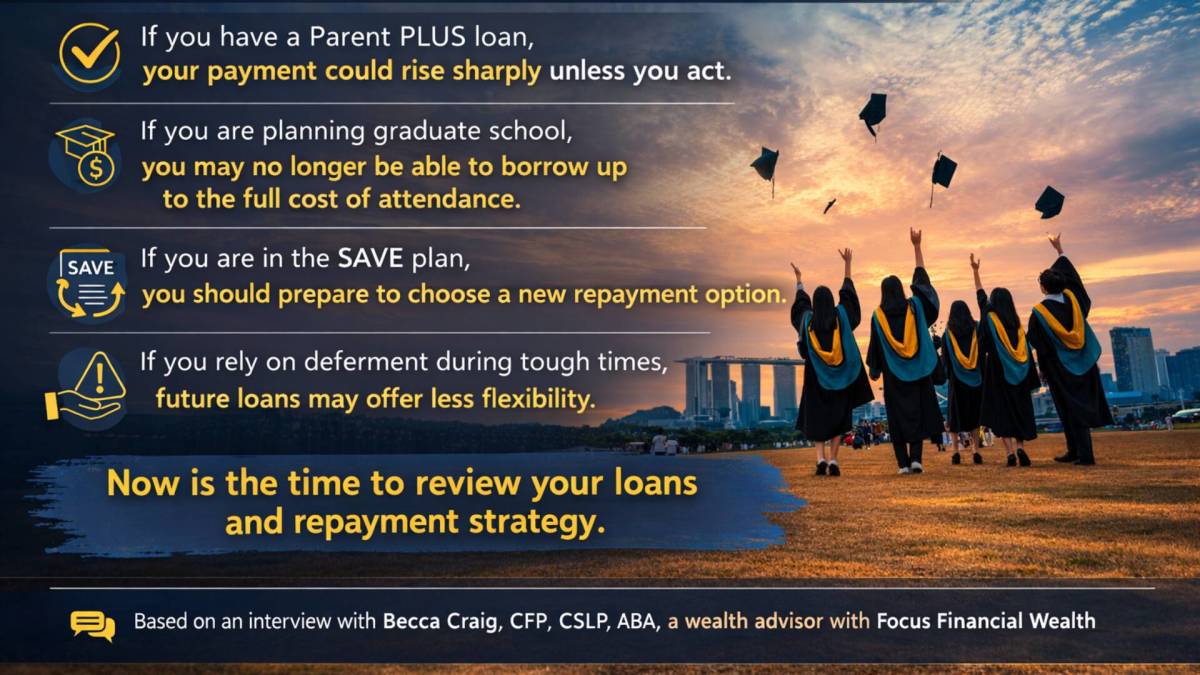

Millions of federal student loan borrowers may soon face higher monthly payments and fewer repayment protections.

The Department of Education has proposed sweeping changes under the Reimagining and Improving Student Education, or RISE, rule. If finalized, the changes would eliminate Graduate PLUS loans, restrict Parent PLUS repayment options, and tighten deferment rules.

Parent borrowers could lose access to income-driven repayment as early as July. Graduate students would face strict borrowing caps beginning in 2026. Borrowers enrolled in the SAVE plan may need to switch repayment programs within the next year.

For households with student debt, this is not theoretical, Becca Craig, a wealth adviser with Focus Financial Wealth, said in an interview. It affects what you can borrow, what you must repay, and how flexible your loan will be during financial hardship.

Below is a transcript of that interview, edited for clarity and brevity.

Pang Yuhao on Unsplash

Proposed federal student loan changes you shouldn’t ignore

Robert Powell: The Department of Education recently released proposed rules that could significantly affect federal student loans. Borrowers shouldn’t ignore them.

Here to explain what might be changing, why it matters and what action steps borrowers should consider is Becca Craig, wealth adviser at Focus Partners Wealth. Becca, welcome.

Becca Craig: Thank you so much for having me, Bob. I’m glad to be here.

What is the RISE proposal?

Robert Powell: Before we get into the specifics, can you set the table? These proposed rules are tied to what’s being called the RISE Act or RISE rules.

Becca Craig: Yes. There’s always a lot going on with student loans, but what borrowers — both current and future — should pay attention to right now is the proposed RISE rule, which stands for Reimagining and Improving Student Education.

Also worth reading

- Retirees may want to rebalance as markets broaden, volatility rises

- Why “breaking even” on Social Security is the wrong goal

- The $83,250 secret every solo entrepreneur needs to know for 2026

- Medicare mistakes seniors wish they’d known sooner

- Elon Musk says stop retirement saving: Experts call it ‘nonsense’

- Social Security benefits could drop 7% in 2032

It has gone through committee review and is now open to public feedback. Once that window closes, we’ll see final regulations. For now, this proposal serves as a barometer of where the Department of Education is heading.

It gives borrowers an opportunity to plan ahead — whether they’re repaying loans now or considering taking out new loans for themselves or a dependent.

Parent PLUS loans and income-driven repayment

Robert Powell: One of the key changes involves Parent PLUS loans. What’s happening there?

Becca Craig: The proposed rule runs nearly 100 pages. But one of the most significant provisions affects current borrowers with federal Parent PLUS loans.

Parent PLUS loans are taken out by a parent on behalf of a dependent. Historically, these loans have had higher interest rates and fewer favorable repayment options.

Under the proposal, Parent PLUS borrowers would no longer qualify for income-driven repayment plans.

That’s a very big deal.

For many borrowers, particularly retirees on fixed incomes, losing access to income-driven repayment could mean their monthly payments double or even triple. Without IDR, they would default to the Standard Repayment Plan.

Borrowers who consolidate their Parent PLUS loans into a Direct Consolidation Loan before the effective date could preserve access to income-driven repayment options. Consolidation typically takes four to six weeks.

Robert Powell: And this remains a federal loan, not a private refinance?

Becca Craig: Correct. Consolidation is entirely separate from refinancing. Refinancing moves a federal loan into the private market. Consolidation keeps the loan within the federal system.

Graduate PLUS loans eliminated for new borrowers

Robert Powell: What about Graduate PLUS loans?

Becca Craig: The proposal would eliminate Graduate PLUS loans for new borrowers beginning July 1, 2026.

Instead, borrowing would be limited through the Direct Loan program with strict annual and lifetime caps.

Graduate students would face a $20,500 annual limit and a $100,000 lifetime cap. Professional students — such as those in medical or law programs — would face a $50,000 annual limit and a $200,000 lifetime cap.

Graduate and professional programs can be extremely expensive. Historically, Graduate PLUS covered the full cost of attendance beyond other aid.

Without it, many borrowers may need to turn to private loans, employer support, family assistance or less expensive program options.

New definition of “professional student”

The proposal also introduces a narrower definition of “professional student,” limiting higher borrowing caps to 11 designated professional degree programs.

If a program is not classified as professional under the new definition, students may have lower borrowing limits.

That classification could significantly affect how much federal funding is available — and whether private loans become necessary.

The SAVE plan rollback

Robert Powell: Many borrowers enrolled in the SAVE plan are wondering what happens next.

Becca Craig: This is the question everyone is asking.

SAVE was designed as a more generous income-driven repayment plan with lower payments and an interest subsidy. However, it has faced legal challenges and is now being rolled back.

Borrowers currently in SAVE will need to choose another repayment plan.

Options still available include:

- Income-Based Repayment (IBR)

- Income-Contingent Repayment (ICR)

- Pay As You Earn (PAYE), though it is being phased out

There is also discussion of a future RAP plan, but borrowers cannot elect into that yet.

My advice: Log into StudentAid.gov, review your loans and use the repayment calculators. Compare your options now rather than waiting for potential backlogs or servicing delays.

Safety nets may tighten

Robert Powell: The proposal also affects deferment and forbearance options. What should borrowers know?

Becca Craig: For loans disbursed on or after July 1, 2027, the proposal would remove unemployment and economic hardship deferments. It would also limit certain forbearances to nine months within a 24-month period.

That matters because loan planning isn’t just about when everything goes right. It’s about layoffs, illness, caregiving, business slowdowns — real-life events.

Borrowers may also end up with split eligibility if they have loans from different periods.

Planning is essential

Robert Powell: What’s the bottom line?

Becca Craig: Borrowers need to look at their full financial picture.

Build or strengthen your emergency savings. Understand your repayment options. And if needed, work with a financial professional who understands student loan planning.

This proposal shifts more responsibility to families and borrowers to fund and plan for higher education. That means evaluating the value of a degree, program costs and long-term repayment implications.

There are also Certified Student Loan Professionals who specialize in incorporating repayment planning into a broader financial plan.

You don’t have to navigate this alone.

Related: A simpler way to pass on your home without probate

#Federal #student #loan #raise #payments #millions