People in the United Arab Emirates, including a prominent businessman, are beginning to criticise the US as Iran’s barrage of missiles and drones on Gulf states continues, roiling the region’s financial markets and economies.

The UAE has been among US President Donald Trump’s staunchest allies, pledging about $1.4 trillion in investments and cultivating commercial ties with his family. That relationship appears to have given Abu Dhabi little influence over the conflict.

“Who gave you the authority to drag our region into a war with Iran? And on what basis did you make this dangerous decision?” Khalaf Al Habtoor, a Dubai billionaire and hotel tycoon, said in a post on X on March 5. “You have placed the countries of the Gulf Cooperation Council and the Arab countries at the heart of a danger they did not choose.”

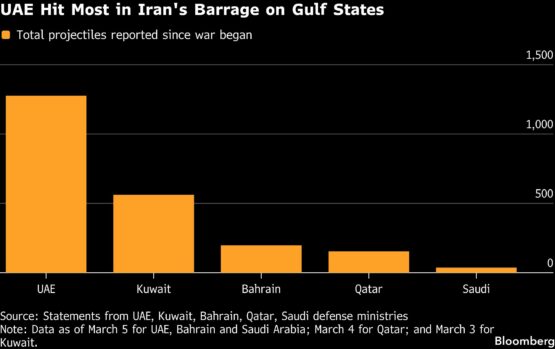

The UAE has faced the brunt of Iran’s retaliatory missile and drone attacks in the Gulf region. While the armed forces have intercepted almost all of the projectiles, the conflict undermines the stability premium that has been a critical part of the Gulf’s appeal for global investors and financiers.

Another leading businessman said the continued instability is pressuring various sectors in Dubai and disrupting supply chains for a range of businesses. If the war stretches beyond a month, some companies will likely face difficult decisions about production and services, he said, declining to be identified discussing sensitive information.

“Most of the Gulf States always knew that President Trump is going to be himself and not necessarily listen to outside influence,” said Ryan Bohl, a senior analyst focused on the Middle East and North Africa at the risk intelligence consultancy Rane Network. “But I think they are taken aback by how willing he is to take risks that impact them.”

The more than 500-word post in Arabic directed at the US president by Al Habtoor, whose portfolio ranges from a polo resort to hotels branded by Hilton and Waldorf Astoria, contrasts with the measured approach taken so far by Emirati officials. Still, it reflects unease among parts of the business community about the potential impact.

ADVERTISEMENT

CONTINUE READING BELOW

Travel and tourism, key pillars of the economy, have been badly hit. Thousands of passengers have been stranded across the Gulf, forcing many onto circuitous, expensive routes to reach functioning airports in Saudi Arabia and Oman. There are tentative efforts to restore service: The UAE is establishing safe air corridors to allow as many as 48 flights an hour.

Dubai’s benchmark stock index, meanwhile, is heading for its worst week since May 2022.

Still, in Dubai and Abu Dhabi, shops and restaurants are open and delivery services are running. Offices are offering work-from-home options, and taxis and public transport are operating, though roads are far less crowded than usual.

Iran has targeted critical energy infrastructure across the Gulf, and traffic through the Strait of Hormuz — a maritime chokepoint vital for energy flows and container shipping — has ground to a near-complete halt, sending crude oil prices surging.

Business leaders and investors are also watching closely for signs that the conflict could begin to affect the Middle East’s overseas investment drive, one of the pillars of its economic strategy.

In addition to the UAE’s commitments, which came as Trump toured the region last year, Qatar and Saudi Arabia had also pledged investments of nearly $2 trillion into the US. These countries have also continued to face waves of missile and drone strikes from Iran.

Now, some Gulf officials are reconsidering major foreign investments as they weigh the potential cost of a prolonged war, the Financial Times reported this week.

ADVERTISEMENT:

CONTINUE READING BELOW

Executives at an Abu Dhabi sovereign wealth fund said no reviews are currently underway, while another investor said the city remains fiscally strong. Still, any pullback could ripple through deal markets that have come to rely on capital from the region.

Commercial ties

Besides the 10-year, $1.4 trillion investment commitment to the US announced last March, Emirati entities have aligned themselves closely with the Trump administration’s priorities, backing artificial intelligence partnerships, and pledging multibillion-dollar energy investments and aircraft orders.

The commercial ties extend to the president’s family. Alongside a partner, the Trump Organization is developing a new tower in Dubai, in addition to projects in Saudi Arabia and Oman. Meanwhile, Abu Dhabi’s MGX took a $2 billion stake in Binance, using a stablecoin tied to the Trump family.

Whatever the criticism of Washington, there’s widespread anger over Iran’s attacks. These came despite the UAE and other Gulf states preventing American and Israeli forces from using their territory or airspace for strikes on Tehran. On Saturday, a senior advisor to UAE President Mohammed bin Zayed urged Iran to “return to your senses.”

Some businesspeople have privately said they also worry about the possibility of a prolonged period of low-grade conflict with Tehran.

Against that backdrop, Trump’s decision to go to war with Iran — widely opposed across the region — has prompted questions about the limits of economic leverage in Washington.

“Investment pledges buy access and goodwill,” said Andreas Krieg, a lecturer in Middle Eastern security issues at King’s College London. “They do not reliably buy veto power in Washington in a crisis, especially when the White House thinks credibility and deterrence are on the line or domestic politics rewards escalation over restraint.”

© 2026 Bloomberg

#Trump #faces #criticism #UAE #business #community #Iran #war