Since 1939, the US college basketball season has culminated in an elimination tournament known as March Madness. It is renowned and loved for producing major upsets, as a single nervous performance can send a top-ranked team crashing out of the competition, while an unfavoured team can defy expectations and win national adoration.

For fans, predicting the outcome of the 67 games played over eight rounds is an annual tradition, though no one has ever managed this feat (the closest being 49 correct picks).

Read: How the biggest names in finance make March madness picks

There are three reasons to draw this analogy in an investment column.

Firstly, the name neatly captures the absolute mayhem we’ve seen on financial markets over the last month.

Secondly, in Gulf War III, if we may call it that, the underdog is outperforming the top seed.

Thirdly, there is a lesson in the limits of prediction, whether you are a sports fan, military strategist or the Average Joe investor.

Market mayhem

In terms of the market reaction, the numbers speak for themselves.

March was not quite over at the time of writing, but the declines have been dramatic.

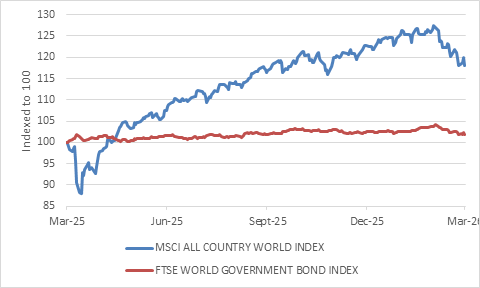

Notably, from a global point of view, bonds and equities fell in tandem.

It is understandable that equities, the riskier asset class, would suffer when there is global anxiety, but the bonds of rich countries normally rally in a crisis.

The problem this time is that investors are worried about the inflation risks of higher oil prices, and potentially also about additional fiscal strain as governments potentially spend more on cushioning their populations from the energy shock and increase in defence outlays. The threat of central bank interest rate hikes also put pressure on bond markets, especially in Europe.

Global bonds and equities in US dollars

Source: LSEG Datastream

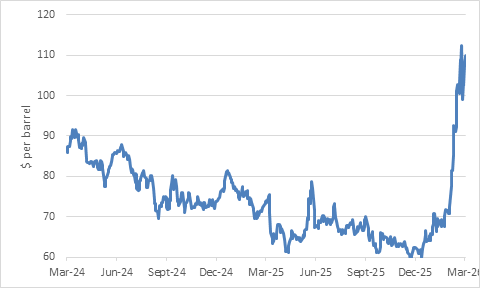

While the oil price has surged by almost 50% to the highest closing level since 2022, gold fell by 14%.

Though movements in the gold price are always a bit of a mystery, clearly some of the more speculative buyers have been spooked.

ADVERTISEMENT

CONTINUE READING BELOW

It also makes sense that investors needing to raise cash would take profit from an investment that experienced spectacular gains over the previous year. This could include central banks needing to protect vulnerable currencies, as reported in the case of Türkiye.

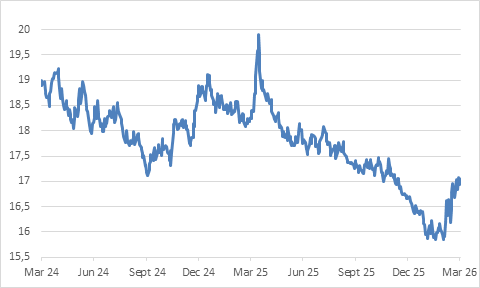

Other precious metals are also weaker, which, together with rising global risk aversion, saw the rand losing ground against hard currencies.

From the point of view of South African investors, global bonds and equities were largely unchanged in the month, thanks to the declining rand. This again highlights the value of portfolio diversification.

Rand-dollar exchange rate

Source: LSEG Datastream

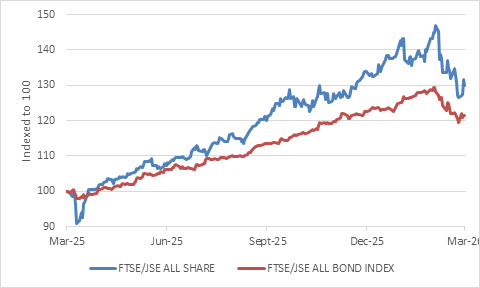

However, it has been a particularly rough month for South African bonds and equities.

Domestic government bond prices fell sharply, leading to higher yields. This follows developments on global bond markets and reflects concerns (likely premature) that the South African Reserve Bank could be raising interest rates, whereas a few weeks ago the expectation was for two to three rate cuts in 2026.

Read:

Sarb holds rate steady at 6.75%

Sarb ties SA rate path to Iran war timeline

Ramaphosa courts investment as South Africa faces Iran war headwinds

The year-to-date returns on the FTSE/JSE All Bond Index are now in negative territory, though longer-term gains are still solid.

The FTSE/JSE All Share Index faced double-digit losses for the month, which will pull first quarter returns into negative territory.

Apart from the general rise in risk aversion, there are sector-specific issues.

Resources shares have taken a beating as precious metals prices pulled back, while higher bond yields have weighed on financials. Nonetheless, the SA equity benchmark is still up more around 30% over the previous 12 months. This is still ahead of cash and inflation.

South African bonds and equities in rand

Source: LSEG Datastream

While the current geopolitical situation is unusual – though perhaps something we should get used to this with three more years of Donald Trump in the White House – market corrections are not.

Part of the long-term upside equities offer is that there will be drawdowns along the way, where the benchmark can drop 10% or 20% (or more).

ADVERTISEMENT:

CONTINUE READING BELOW

It is tempting to think that those declines can be avoided. However, timing the market is tough, since there are two big calls to be made: sell at the right time and then buy back again. It is the second leg of the trade that is often more difficult. By the time the ‘dust has settled’ the market has rallied already.

When it comes to economic recessions, for instance, the equity market tends to turn about three to six months before the economy does. Markets look ahead, and they will do so again in this instance.

Game theory

In the meantime, the situation remains fluid and volatility is set to endure. While the path ahead is uncertain, it can be useful to consider the incentives facing the different players in this geostrategic game.

Henry Kissinger once noted that in an asymmetric battle the conventional army loses if it does not win, while the guerrilla force wins if it does not lose.

Iran is not fighting a guerrilla war, but the principle is the same.

The US has overwhelming superiority in conventional military terms, and together with Israel, has destroyed Iran’s navy and air force. But everyday Iran holds on might be seen as winning.

It has managed to shut the most important waterway in global energy markets by shooting only a handful of missiles and cheap drones, causing the price of oil to surge, and inflicting political pain on the US, with voters in the November mid-term elections likely to respond angrily to higher gasoline prices.

Whatever trust there was between Iranian leaders and their US counterparts was shattered when attacks started while negotiations were still underway in February. This is surely an obstacle to a peace agreement. Iran will fear that Israel and/or the US will attack again in future as soon as it lets its guard down.

The ability to close the Strait of Hormuz gives it deterrence to future attacks but will also add greatly to the sense of unease in the region. Can this be acceptable to the US and the other Gulf states in particular?

Nonetheless, even though Iran has held out longer than the US and Israel expected, it had a very weak economy and unpopular leadership to begin with, so its ability to keep fighting is not infinite.

As much as we worry about inflation in the rest of the world, official inflation rates in Iran were above 40% before the war broke out.

Shortages and disruptions mean it will be much worse now, even if Iranians don’t pay market prices for fuel. The risk to internal stability is surely as much of a concern to the regime as fighting externally.

Read:

Iran attacks Kuwaiti oil tanker as Trump expands US threats

No April Fools’ joke: Diesel still rockets over R7/l, petrol over R3/l

Moreover, since the oil price spike will hurt developing nations the most, countries like India and China and indeed South Africa have every reason to push for peace.

Pakistan has already stepped forward as a mediator. In turn, Iran appears ready to let ships pass through the Strait of Hormuz if they are not linked to the US and its allies and are prepared to pay a passage fee.

The bottom line is that the conflict is far from over and may still escalate.

ADVERTISEMENT:

CONTINUE READING BELOW

However, if an uneasy truce can be reached in the next few weeks, the damage to the global economy will be limited and markets can bounce back. If it drags on for months, the risk increases that interest rates hikes and weak markets will exacerbate the pain at the petrol pump.

It is therefore a positive development that US President Trump is seemingly trying to de-escalate. He has a strong incentive to do so but is also sending mixed messages by increasing the presence of US troops in the region.

Will Iran take the opportunity to also dial down the temperature? And can other Gulf states live with an Iranian neighbour that is wounded but still on its feet? There are more questions than answers.

Brent crude oil, dollars per barrel

Source: LSEG Datastream

Unpredictable

Finally, the folly of predictions, closely linked to overconfidence.

The Trump administration apparently failed to understand that the situation would escalate to this extent, even though geopolitical analysts have fretted over the closure of the Strait of Hormuz for decades. Iran’s actions were predictable. What happens next is not.

This means that any portfolio change based on the expectation of a single outcome materialising, good or bad, is risky.

If your portfolio was appropriately positioned prior to the war, there should be no reason to make any sudden changes now.

Indeed, any changes in investment strategies should ideally be driven by changes in personal circumstances, not market conditions.

As a final thought, the war is obviously generating many upsetting headlines. Not everything you read on social media is true, especially with convincing but fake AI-generated content circulating.

Be very careful about making financial decisions based on the news or social media stories, including reports about fuel shortages. The media thrives on clicks and engagement and has every incentive to keep you engaged.

Remember, you have the option of doing nothing, which still counts as doing something.

Izak Odendaal is an investment strategist at Old Mutual Wealth.

#March #madness