From a conference room atop H&M’s headquarters in the heart of Stockholm – with its brown-toned wood and clean lines giving the space a distinctly Scandinavian feel – chief executive Officer Daniel Ervér speaks of reviving the one-time Swedish highflyer. What he’s up against is a credibility problem.

Eight years ago, after a record quarterly sales drop, Hennes & Mauritz AB’s then CEO Karl-Johan Persson, a scion of its billionaire founding family, had gathered shareholders in the historic Stockholm concert hall Cirkus for its first – and only – capital markets day to reassure them that things would get better. They didn’t. Just weeks after the event – where Persson had cut a dapper figure, tie-less, in a white shirt and an Arket suit – the company dumped more bad news: roughly $4 billion in unsold garments and a 62% drop in operating profit.

Read: How Shein and Temu have gobbled market share from SA retailers

Shein’s robust US growth evaporates after Trump tariff hit

Now, Ervér – who took over in 2024 – is seeking once again to convince investors that the group has turned a corner. Alongside an ambitious remake, Ervér has sought to dig H&M out of one of the biggest inventory pileups in modern retail. While those efforts are bringing richer operating margins and profits, they have yet to lead to sustained sales growth, and Ervér is asking for patience.

“We have begun to lay a stable foundation for future growth,” the 44-year-old Swede, a quintessential insider who’s spent his entire career at the company, said in an interview on April 1. “That can be seen in increased profitability, better cash-flow earning capacity, lower inventory levels… Over time that will lead to us seeing stronger growth. I think we are at the beginning of the journey, but it is a long-term journey.”

Time is something investors are reluctant to give the company. From its 2015 peak, H&M has lost roughly half its market value, erasing tens of billions of dollars in equity. Just two years earlier, it had been Stockholm’s most-valuable listed company.

An H&M store in Shanghai. Chinese ultra-low-cost rivals like Shein and Temu have reset the market. Image: Qilai Shen/Bloomberg

ADVERTISEMENT

CONTINUE READING BELOW

H&M’s inability to stack up in the $1.9 trillion global apparel market against Zara-owner Inditex SA on the higher end and an onslaught from cutthroat price-driven competitors like Shein and Primark means investors are unwilling to bite. And there’s little to suggest that trend will be reversed anytime soon – H&M’s sales on a constant currency basis slid 1% in its first quarter.

“I think the margin improvement that H&M has managed to achieve under Ervér is impressive, but I still miss growth at the company,” said Lars Soderfjell, head of Nordic Equities at Finland’s Alandsbanken Abp. “The big question is whether H&M is still relevant to its core customers – women aged 15 to 30.”

H&M was slow to grasp the structural changes in the industry, which were transformed dramatically in the last decade by digitalisation. Without the need for a physical store, hundreds of new competitors popped up, changing the retail landscape entirely.

Ervér says the steps he put in place are helping H&M deal better with the new environment. He whittled away layers to take decisions faster, streamlined the number of suppliers, bringing more of them closer to Morocco and Egypt from China and Bangladesh – and got designers to scale up products. That’s helped bring down H&M’s inventory-to-sales ratio to the lowest level in 10 years, and prepared it to better take on “brutal, tough competition, and competitors that come from all directions,” he said.

“We have higher ambitions for growth over time – to drive both our customer value and shareholder value – by starting to grow more than we have done in recent years,” he said.

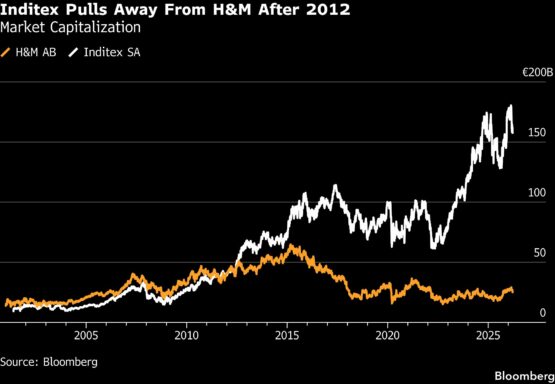

A decade ago, H&M and Inditex were seen as peers. The two generated broadly comparable earnings in the early 2010s. In market value, however, Inditex started to break away after around 2012.

ADVERTISEMENT:

CONTINUE READING BELOW

By 2016, growth at the Spanish group took off while H&M fell behind. The gap widened further in the years that followed, particularly after the pandemic. Inditex’s margins rebounded strongly and remained structurally higher as its more nimble model helped it pull ahead. Today, Inditex has roughly five times H&M’s profit. While Ervér has struggled to revive operating margins to 10%, Inditex’s are closer to 20%.

After a decade of missteps, investors want H&M to show it can sell more at full price, avoid inventory pileups that force fire sales and sharpen its brand – all while competing with ultra-cheap online rivals and an increasingly upmarket Zara.

On Ervér’s watch, inventories have come down sharply and online operations now account for roughly 30% of sales. Store numbers have been slashed 19% from their 2019 peak, including the closure of all 130 acquired Monki shops. The core H&M brand has 832 fewer stores, with consolidation into larger flagship-style outlets – a newly renovated store on Stockholm’s Hamngatan, just blocks away from its headquarters, is set to reopen soon.

But all that may still not be enough, says Charles Allen, a Bloomberg Intelligence analyst. “Inventory days are still above 130, which is much higher than they were historically and compare unfavorably to Inditex, which is below 90,” he said. “So this suggests there is still some excess inventory. On balance I think there is more clearance to be done.”

In its report The State of Fashion 2026, consulting firm McKinsey places H&M in the value segment, alongside players such as Uniqlo. The report also points to a broader shift across the industry: value brands are upgrading their offer to compete with ultra-low-cost rivals like Shein and Temu, while mid-market players such as Zara are leaning into “affordable aspiration,” with a stronger focus on design and quality.

“Fundamentally, Inditex has pulled ahead of H&M by having a higher degree of its own production located closer to the customer, meaning shorter time-to-market,” said Soderfjell. “Much of what H&M has done in recent years has been to move closer to the Inditex model, but is that enough to regain the positions they have lost?”

ADVERTISEMENT:

CONTINUE READING BELOW

How H&M navigates that balancing act will depend in large part on the Persson family, which has been steadily accumulating an ever-increasing stake in the company. With a net worth of about $23.4 billion, according to the Bloomberg Billionaires Index, the family now controls more than 86% of H&M’s voting rights – sparking speculation that the company will eventually be taken private.

“I don’t want to speculate; I think very little about that question,” Ervér said. He said he works closely with the family and is in regular contact with Karl-Johan Persson, who served as CEO until 2020. “We meet every week, and we talk on the phone several times a week,” he said.

As international investors have thinned out, the company has become more tightly held, with limited external pressure to force faster change. That gives H&M unusual latitude for a listed retailer. It can invest in supply-chain changes and brand repositioning over a longer horizon, without the pressure to deliver immediate results. But that double-edged sword also removes an external catalyst for more radical action.

The key question is not whether H&M can change, but how quickly. A decade after it first fell behind Zara, the company has stabilised. The next phase will determine whether it can do more. As supply chains are reshaped and competitive pressures intensify, H&M’s ability to balance speed, price and brand will determine whether it can grow and rebuild margins – or remain stuck between the two ends of the market.

“We are doing a very long-term, extensive job of building a stronger H&M,” Ervér said.

Investors, meanwhile, are saying: show me.

© 2026 Bloomberg

#Swedens #top #company #HMs #struggling #sell #rebound #story