A fortnight ago, in Levi’s is not the next Nike, I touched on Nike’s steady collapse from fatal decisions made in building its direct-to-consumer (DTC) business.

I will now focus on how Levi Strauss & Co differs.

As evidence of Levi’s success, in April the group published a strikingly good quarterly report and even upgraded its own guidance:

- Net revenues grew 14% year on year and organic revenue was up 9% year on year, with management noting volumes growth and price growth across the board (a really health sign!);

- Diluted earnings per share (EPS) and adjusted EPS followed to grow 28% and 11% year on year respectively; and

- Revenue growth guidance was effective hiked by 0.5% and EPS guidance effectively hiked by a further 2% year on year .

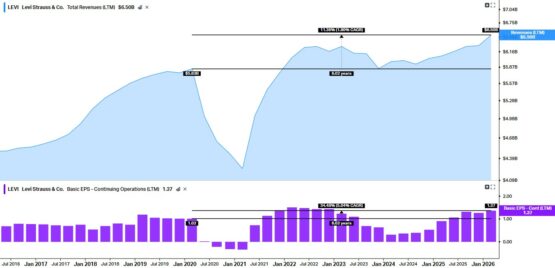

Levi’s revenue and EPS (12-month rolling to adjust for seasonality inherent in clothing)

Source: Koyfin

While Covid-induced volatility took a while to normalise, tracking Levi’s 12-month rolling sales makes it clear that the group is steadily growing (see chart above).

From tracking just before Covid, the group has ground out a revenue compound annual growth rate (CAGR) of 1.8% year on year and an EPS CAGR of 5% year on year (the latter driven by good operating leverage).

Levi’s DTC sales have grown from 42% of group revenues in Q1/2020 (just before Covid broke out) to 52% of group revenue in Q1/2026. In this latest quarter, DTC grew 16% year on year.

ADVERTISEMENT

CONTINUE READING BELOW

How is this happening?

But following on from my prior article chronicling Nike’s DTC-induced collapse, how is Levi’s managing to grow DTC while maintaining its other sales?

And how is it doing so in the hyper-competitive denim/jeans category?

Firstly, there are the subtleties of Levi’s product expansion (including expanding its portfolio from bottoms to now include tops) versus Nike’s innovation recession (see previous article).

Then there’s the fact that Levi’s is leaning into culture (see Beyonce’s unsponsored song named after it!) while Nike leant into data and apps.

Finally – and most importantly – the major difference in their DTC strategies is that while Nike tried to pivot into ‘DTC-only’, Levi’s focused on ‘DTC-first, but not DTC-only‘.

Read:

Nike lays off 775 workers as it boosts use of automation

Adidas lifts profit target as Samba boom withstands tariffs

Levi taps Victoria’s secret executive to run global supply chain

Nike’s mistake was to view wholesalers and retailers as a “frictional cost” to cut out – but when it did cut them out, it created whitespace for its competitors to fill and gave them consumers to try their product.

The rest is history and Nike lost the consumer.

ADVERTISEMENT:

CONTINUE READING BELOW

Levi’s, under CEO Michelle Gass, treats its wholesalers as vital infrastructure for discovery.

While the group prioritises its own Levi’s (and Beyond Yoga) stores, it has maintained healthy relationships with high-end retailers and department stores.

This is clearly evidenced in the Q1/2026 results, where DTC grew 16% (as noted above) and its wholesale revenues increased 12%.

The latter point here is key: Wholesalers bought more from Levi’s, not less.

All this may sound too subtle to matter, but these are very volume-sensitive business models. Nurturing all routes to market while maintaining discipline in product quality, innovation and brand-building is important.

Likewise, getting even one of these aspects wrong can have dramatic and hard-to-reverse consequences (see chart below).

Levi Strauss versus Nike share price

ADVERTISEMENT:

CONTINUE READING BELOW

Source: Google Finance

To conclude, I was wrong on Levi Strauss & Co.

Listen/read:

Is Levi Strauss the next Nike? [Aug 2021]

Last Levi’s factory standing [May 2016]

Levi’s is not the new Nike, thankfully. It appears to have learnt from Nike’s calamitous mistakes in building a critical (but risky) DTC (only) business channel.

Rather, Levi’s is charting its own DTC and omni-channel strategy that has a far more balanced approach – and given its mere $8-9 billion market cap versus Nike’s $65 billion, it may have a lot more runway to grow into.

* Keith McLachlan is CEO of Element Investment Managers.

* McLachlan and portfolios managed by him may hold Levi’s shares.

#Levis #Nike #Part