During the first three months of 2026, global debt rose by 7.7% year on year, an increase of $25.1 trillion, taking the total level of debt to a record high of $352.7 trillion.

Most of the world’s debt (69.7%) is owed by developed economies, especially the United States, which accounts for 30% of global debt.

Listen: Avoiding the debt trap: Household conversations you should be having

However, the growth of debt in emerging markets (which now totals $106.7 trillion) continues to outpace that of developed markets, rising by 9.9% over the past year and by an annual average of 12.4% over the past 30 years. This compares with growth of 4.9% for developed economies over the same period.

Within this context, South Africa represents an insignificant 0.24% of global debt, although this is largely irrelevant to this discussion.

SA’s debt totalled $835.1 billion in Q1 2026, which is only 0.8% of total emerging market debt, and has risen by a modest annual average of 6.7% over the past five years.

Nevertheless, compared with 60 emerging markets, South Africa is the eighth most indebted emerging market.

Around 43% of SA’s total debt is owed by the government, which, at 78.8% of GDP in Q1 2026, is relatively high when compared with other emerging economies, placing SA government debt as the 15th highest on the list of 60 emerging economies.

ADVERTISEMENT

CONTINUE READING BELOW

Read:

Rate cuts and two-pot relief fail to stop SA’s debt spiral

Expectations grow for SA credit ratings upgrades

Expectations grow for SA credit ratings upgrades

It is also well documented that SA government debt has become increasingly less affordable in recent years, with debt servicing cost rising to over 20% of total tax revenue

However, more recently, the National Treasury has made meaningful progress in controlling SA’s fiscal deficit, generating a primary budget surplus in each of the past three years, as well as focusing on the quality of government spending and not just on the overall level of spending.

Read: Tars to root out government ghost workers

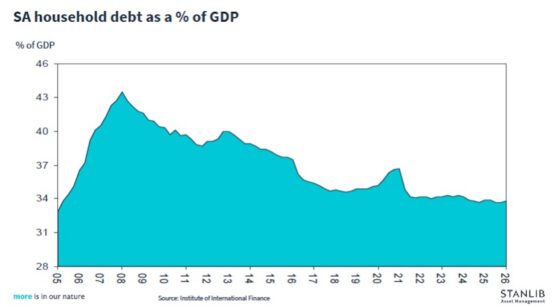

In contrast, SA’s household debt is much more manageable at 33.8% of GDP, or only 18.2% of total South African debt.

Furthermore, household debt reached a record high of 43.5% of GDP in Q1 2008 and, over the past 12 years, has generally moderated as a percent of GDP (see chart below).

Source: Institute of International Finance

However, when measured against 60 emerging economies, SA’s household debt ranks as the tenth highest.

This relatively high ranking likely reflects a combination of two key factors:

ADVERTISEMENT:

CONTINUE READING BELOW

- First, the sophistication and growth of SA’s financial system, especially within the banking sector, has helped to broaden the adoption and use of credit. This, coupled with the availability of store credit and other forms of finance – for example, the recent rapid growth in buy now, pay later (BNPL) facilities – means that the household sector’s use of credit facilities has expanded meaningfully over the past few decades, outpacing many other emerging markets despite the underperformance of SA’s labour market.

- Second, South African households have a high propensity to consume, encouraged by the wide array of goods and services that are readily available, including the growth of online shopping. Stated differently, households have very low levels of discretionary savings. Added to this, high unemployment means that the dependency ratios within most families are extremely high, resulting in many households having to use credit to fund unexpected or irregular expenses.

Fortunately, the household sector’s debt-servicing cost remains manageable (albeit on the high side) at 8.4% of disposable income.

Historically, SA households tend to experience significant financial stress when debt-servicing costs rise above 10% of disposable income.

It also means that if the current increase in inflation (which is currently driven mainly by fuel prices) begins to spread to other goods and services, the outlook could change significantly.

If this broader inflationary pressure forces the South African Reserve Bank (Sarb) to systematically raise interest rates over the next few quarters, SA households will start to experience significant financial stress, likely resulting in a meaningful increase in bad debts.

Equally, if SA can eventually make progress towards embedding the new 3% inflation target, the Sarb should be able to lower SA interest rates on a sustained basis.

This would reduce some of the financial pressures most households currently experience, as well as lower the cost of capital required to funds SA’s long-term economic growth and development.

* Kevin Lings is chief economist at Stanlib.

#SAs #household #debt #compare #globally