Novo Nordisk has long been a core holding for quality-focused institutional investors, having dominated the global insulin market for more than a century.

However, its evolution from a diabetes specialist to a leader in weight loss therapies has fundamentally reshaped its valuation and growth profile.

This shift was driven by drugs that mimic glucagon-like peptide-1 (GLP-1). Originally developed to improve glucose control for diabetics, these drugs revealed a powerful secondary effect: significant weight loss.

GLP-1 slows gastric emptying, prolonging the sensation of fullness while signalling satiety in the brain. This dual mechanism positioned Novo Nordisk as a first mover in pharmacological treatments targeting the global obesity epidemic.

Novo Nordisk’s key innovation was semaglutide: a synthetic drug designed to mimic and amplify the effects of GLP-1 in the body on a more sustained basis. Marketed as Ozempic in 2018 for diabetes and later Wegovy for obesity, semaglutide became one of the fastest-growing pharmaceutical products in history.

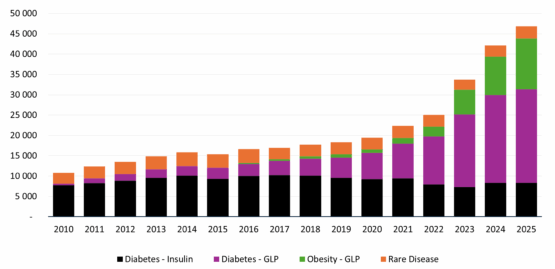

The chart below shows the exceptional growth in revenue contribution from the GLP-1 therapies.

Novo Nordisk revenue contribution by segment (USDm)

Source: Novo Nordisk

Prior to the ‘Ozempic era’, Novo Nordisk epitomised the ‘quality’ factor in many quantitative investment frameworks.

Between 2008 and 2018, the company delivered steady growth (9% sales compound annual growth rate and 15% earnings CAGR), exceptional profitability and shareholder returns (return on invested capital of 42%).

This combination of robust growth, exceptional returns on capital and shareholder-friendly capital allocation made Novo Nordisk a textbook example of a high-quality compounder.

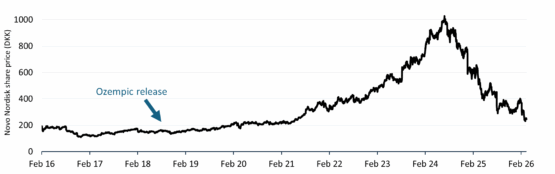

Valuation reset creates opportunity

By 2024, strong share price performance (approximately 40% annualised over six years) had pushed valuations to elevated levels.

A sharp correction followed after missed analyst expectations and subsequent downward revisions to guidance, with the stock declining by approximately 60% from its peak by April 2025.

This correction compressed the one-year forward price-to-earnings (PE) multiple (from 35 times to a compelling 15 times).

This reset created an attractive entry point.

Novo Nordisk valuation reset

Source: Bloomberg

Given a compelling valuation, Truffle invested in Novo Nordisk during April to June 2025, based on several factors:

Massive addressable market: Only 2% of the world’s 768 million obese individuals were receiving pharmacological treatment and the market was expected to grow from $30 billion to $120 billion.

Limited competition: Novo Nordisk and Eli Lilly were dominating a fast-growing duopoly.

Potential beyond weight loss: GLP-1 drugs also demonstrated broader health benefits, including cardiovascular and metabolic benefits.

Compounders to be eliminated: The expected regulatory crackdown on ‘compounders’. These are unregulated entities permitted to mass-produce copycat drugs during FDA-declared shortages.

Pricing pressures offset by volume: Headwinds of net pricing compression, particularly from Pharmacy Benefit Managers (PBMs) and negotiated higher rebates under government pricing frameworks were offset by sheer volume growth from expanded access.

Significant barriers to entry: The capex barrier to reach scale was extremely high.

Valuation provided asymmetry: At the time of investing, we believed the market was underestimating Novo’s earnings potential.

Given the risks around longer-term pricing, competitive dynamics and compounder risks, we sized the position in our global funds modestly, while continuing to better understand these risks.

What changed?

While we aim to invest for long-term outcomes, a core part of Truffle’s investment process is the continuous reassessment of our investment thesis as new information emerges.

From May 2025, Novo Nordisk issued three downgrades to revenue and earnings before interest and taxes (Ebit) guidance. This prompted a review of the assumptions underpinning our investment thesis as explained below and we subsequently exited our position in November 2025, with the share price down 25% since the time we sold.

Compounders persisted: Although a nominal ban on compounders was introduced in May 2025, federal enforcement was practically non-existent. At the same time, Eli Lilly navigated this environment more effectively.

Capex barriers lower than expected: The rapid proliferation of compounders demonstrated that synthesising the semaglutide active ingredient was less technically demanding than the market had assumed.

Intensifying competition and pricing pressure: Eli Lilly’s dual-agonist (GLP-1/GIP) demonstrated superior weight loss outcomes in real-world data, accelerating share gains in the branded segment. Meanwhile, generic manufacturers in China, India, and Brazil were showing greater promise and scale, threatening Novo’s growth prospects outside the US/EU.

Updated valuation: These structural changes have significantly altered the investment’s risk-reward profile. We revised our medium-term growth assumptions from low teens to single digits. Recognising that the asymmetry had reversed, we liquidated the position in November 2025.

The Novo Nordisk case illustrates why investors should avoid anchoring to an original thesis, even with high-quality companies. Competitive dynamics, regulation and industry structure can change rapidly.

Truffle’s investment process places strong emphasis on continuous debate and reassessment of the core assumptions. This is vital to ensure a position in the portfolio remains justified by current fundamentals and changing outlooks rather than past performance.

In many cases, quality businesses require more scrutiny; their strong track record can mask emerging risks such as pricing pressure or erosion of competitive advantages.

AUTHOR: Danesh Ranchhod | Equity analyst at Truffle Asset Management

Ranchhod joined Truffle in March 2025 as an equity analyst covering global stocks. Danesh brings a wealth of experience in research, having worked as an equity analyst at Franklin Templeton Emerging Markets for 14 years, covering companies in South Africa and Frontier Africa across various sectors. He began his career as a performance and attribution analyst, first at JP Morgan Administration Services and then Investec Asset Management (now Ninety-One). He has also worked as a buy-side trader for RECM and in roles across operations and investments at Optis Investment Management.

Disclaimer

Truffle Asset Management (Pty) Ltd is a registered Financial Services Provider (FSP Number: 36484). Registered for Categories I and II. This document does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorised or to any person to whom it would be unlawful to make such offer or solicitation, and is only intended for the use by the original recipient/addressee. If further distributed by the recipient, the recipient will be responsible for ensuring that such distribution does not breach any local investment legislation or regulation.

Prospective investors should inform themselves and take appropriate advice on any applicable legal requirements, taxation, and exchange control regulations in the countries of their citizenship, residence or domicile that might be relevant to the subscription, purchase, holding, exchange, redemption, or disposal of any investments.

Opinions expressed are current opinions as at the date appearing in this material only. The information is confidential and intended solely for the use of Truffle’s clients and prospective clients, and other specific addressees. It is not to be reproduced or distributed to any other person except to the client’s professional advisers.

While the information obtained is from sources we believe to be up to date and reliable, Truffle does not guarantee its accuracy or completeness. Truffle does not accept any liability for inaccurate or incomplete information contained, or for the correctness of any opinions expressed. Past performance is not an indication of future performance.

info@truffle.co.za | +11 035 7337 | truffle.co.za

Brought to you by Truffle Asset Management.

Moneyweb does not endorse any product or service being advertised in sponsored articles on our platform.

#Truffle #bought #sold #Novo #Nordisk