The war in Iran has dealt a blow to one of Wall Street’s favourite trades: emerging markets.

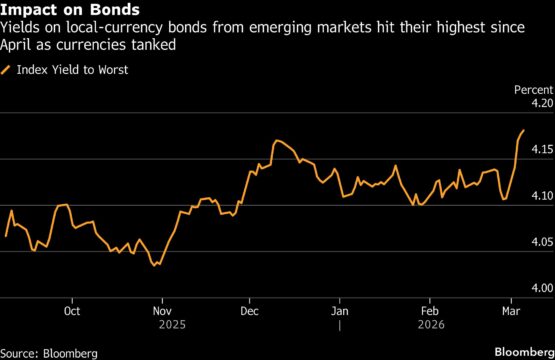

Stocks and currencies have seen steep losses, with the MSCI equity index posting its biggest weekly drop in six years, and bond yields have jumped. Even so, money managers at firms including Pacific Investment Management Co, Barings and T Rowe Price Group Inc. argue the longer-term case for emerging markets remains intact. While some are tweaking portfolios at the margins, most are holding off on major shifts for now.

Their conviction rests on what investors see as the main drivers behind the emerging-markets rally: a push to diversify from US assets, attractive valuations and solid economic growth. Many believe those themes will reassert themselves once the geopolitical shock fades, and fund flows suggest investors are taking advantage of the dip in prices to buy more securities. Investors added $12.6 billion to emerging-market stocks and bonds in the week through Wednesday, according to a Bank of America Corp. report, citing EPFR Global data.

ADVERTISEMENT

CONTINUE READING BELOW

“We’re waiting for more clarity,” said Nick Eisinger, the head of EM sovereign credit strategy at JPMorgan Asset Management. “We like the fundamental story across a lot of EM, but unfortunately, the fundamental stories don’t really count for very much right now, so we need this shot to pass.”

Still, the risks are mounting, with Brent crude surging past $90 a barrel and conflict across the Middle East intensifying. The worry is that soaring oil prices will pressure economic growth in countries that rely on imports. As well, a stronger dollar — which has re-emerged as the haven trade of choice — tends to tighten financial conditions and erode returns for emerging-market investors.

ADVERTISEMENT:

CONTINUE READING BELOW

JPMorgan Chase & Co. cut its recommendations on emerging-market assets three times in the past week, with uncertainty clouding the outlook for the asset class. The bank’s strategists slashed bullish calls to marketweight on foreign exchange and local rates, and moved to tactical underweight positions on sovereign and corporate dollar bonds.

Here’s what other investors see ahead for the asset class. The comments have been edited for length and clarity.

Don’t get too panicked

Bill Campbell, a portfolio manager at DoubleLine Group LP

I’m not in the camp that this fundamentally changes everything, that it’s time to close out all emerging markets. I’m much more in the camp that this is an exogenous shock. As of now, my expectation is it should be contained. In that case, it doesn’t change, a priori, the conditions of a supportive global growth backdrop, EM-DM convergence, and the worries about fiscal and term premium in developed markets. Also, in a world where valuations remain extremely tight, emerging markets offer a lot of value and diversified ways to play investment themes.

If you look across what happened across markets, it was heavily held trades that unwound. So we have some cleaner positions now, and if we get some clarity or some more line of sight on the Iran situation, this could be a fantastic spot to re-engage in EM currencies and EM local rates. I’m trying not to get too panicked and I’m trying to look for opportunities.

This cycle is different

Pramol Dhawan, head of emerging markets portfolio management at Pimco

We are currently seeing one of the key risks play out in real time, that of geopolitical friction. Against that, what will continue to sustain emerging markets over the longer term is continued fiscal credibility at the sovereign level, further evidence that EM central banks have anchored inflation expectations durably, and continued rotation by global allocators, who remain underweight EM relative to fundamentals. The current EM cycle appears more durable than previous rallies, including the 2008 cycle.

The diversification argument

Ghadir Cooper, global head of equities at Barings

Geopolitical risk obviously affects all markets not just EM. High oil prices, if persistent, will have a detrimental effect on all energy-importing countries.

ADVERTISEMENT:

CONTINUE READING BELOW

There is a powerful combination supporting emerging markets going forward — attractive valuations and it is what we believe a very under-owned asset class, not represented enough in portfolios. EM policymakers have typically been far more fiscally prudent than developed peers. Given that EM has underperformed for over a decade and given the relative attractiveness of the asset class, a diversification argument is forming — out of US assets into international and EM.

Reducing gulf exposure

Eric Fine, head of emerging-markets active debt at VanEck Associates

Gulf bond spreads are largely unchanged, yet risks have clearly risen. Spreads of the key countries (UAE, Qatar, Saudi, and Kuwait) are sub-100 basis points over Treasuries, so reducing that exposure is pretty straightforward as there are other alternatives without proximity to the conflict.

EM local currency got cheaper so we increased some exposure, which we reduced before the conflict because they had become too frothy. South Africa, for example. We increased Colombia and Chile as well. EMs in the bond world are generally commodities exporters. Latin America and sub-Saharan Africa, in particular have winners. Asia will be challenged economically, but external accounts and policies are so strong, anchored by an appreciating Chinese yuan, so opportunities exist there too.

The only metric that matters for now is conflict duration. If the market keeps increasing its conflict duration estimates, they will start to increase global recession odds. But note that commodity prices are likely to remain high, so EM commodities exporters aren’t obviously vulnerable in this outcome.

Switch to higher quality

Samy Muaddi, head of emerging markets fixed income at T Rowe Price

EM foundation is quite good right now, so it’ll likely survive the latest bout of risk aversion. But the combination of higher oil prices and looser US fiscal could contaminate the rates outlook, and I don’t think the market is well positioned for that. Anything that changes core rates, volatility or equity risk is naturally going to end up contaminating emerging markets.

The key question for credit is where spread compression is being earned by genuine policy adjustment, making it more durable. Our rotation into higher-quality, higher-liquidity credits from frontier names, which started last year, had proven to be resilient in face of this week’s selloff.

In local markets, we like countries where there’s no front-loaded election risk in the next three to six months, and where real rates are still high, for instance, Mexico, Romania and Turkey. Latin America is more immune from a financial conditions perspective and should benefit from portfolio rotations.

© 2026 Bloomberg

#Iran #conflict #puts #emergingmarkets #revival #test